Credit data shows: There’s no housing crash coming

The housing bubble crash theory has failed once again as we approach the end of 2024, but it’s always important to know why something didn’t happen. This week, we got the updated New York Fed credit data report and it shows the strong position of homeowners — especially in comparison to the years before the Great Financial Crisis.

This is the kind of information you need as we get close to Thanksgiving and share the dinner table with Uncle Dave who says (for the 13th year) that we’re seeing 2008 all over again. This is the person who says everyone should sell their homes so they can rent while they wait until home prices crash. The typical response is to take Uncle Dave to bed for his nap. However, I will give you all the charts to show Uncle Dave that housing credit doesn’t look like it did in 2008 because the qualified mortgage (QM) law makes that impossible.

Foreclosure data

The chart below shows that the 2008 housing crisis started years before the 2008 recession. The credit markets were toxic back then, featuring loans with big recast payments which meant that you could have two people working full-time and still be at a credit risk. As you can see in the chart below, the credit markets broke in 2005, 2006, 2007 and 2008, and then the job-loss recession of 2008 started, which made things much worse.

None of that action has been happening for 14 years because the credit market changed after the 2010 qualified mortgage rule. Now, most loans are 30-year-fixed mortgages and people’s wages rise almost every year. We had multiple refinancing waves in 2012, 2016, 2020 and 2021. Foreclosure data fell quarter to quarter in Q3. Ladies and gentlemen, stop dancing with a ghost.

<\/script>FICO score data

The FICO score data is the sexiest economic data in America — it’s been hot since 2010! As homeowners age, their wages have grown and their cash flow has improved. People buying homes have very high FICO scores — this has always been the case. Thirty-year fixed loans, better underwriting standards and more cash flow mean homeowners are in excellent financial shape, and their credit data shows that.

<\/script>Credit stress data

When the next job-loss recession happens, we will see a rise in credit stress data and I am 100% sure the doomers of America will sit on their useless YouTube and X accounts, pushing their negative narrative nonstop. However, now that you have all the data, you can see that the credit stress data we saw in the 2008 crisis will never happen again as long as we have qualified mortgage in place. My crusade in the last decade was about ensuring lending standards are never eased because standards are already liberal today, but not crazy anymore.

The reason I fought hard for this premise is that when we do have economic stress such as we saw early in COVID-19 and with the big burst of inflation, homeowners will be shielded with their boring vanilla 30-year fixed mortgages.

With the data line below, I anticipated that we would return to pre-COVID-19 levels of credit stress by the end of 2024, but that never happened. Again, everyone pushing housing 2008 needs to snap out of it.

Please use these updated charts on credit data for your Thanksgiving dinner conversation and remember why this is so important. The new listings data we track with Altos Research is trending at the lowest levels ever during the past few years, while back then it was running at accelerated levels. Here is an example with our Nov. 9 data. Look at the difference between this week in 2024 versus the same weeks in 2009-2011. We had a lot of stressed sellers back then!

New listings data this week:

- 2024: 48,863

- 2009: 274,614

- 2010: 359,534

- 2011: 315,915

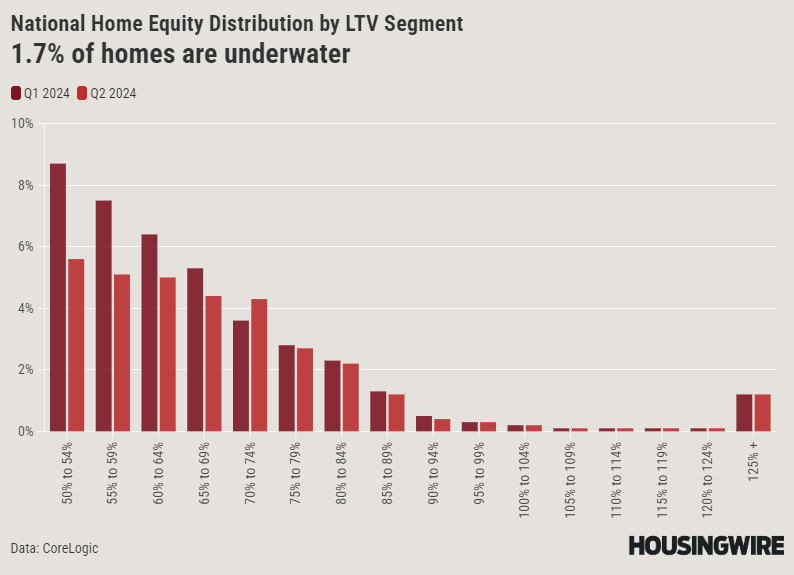

These credit-stressed sellers did not turn around and buy another home, so they created years of elevated distress supply in the marketplace. This hasn’t happened once over the last decade, nor will it until we see a job-loss recession. Also, back in 2010, over 23% of homes were underwater; today, it’s the lowest percentage ever.

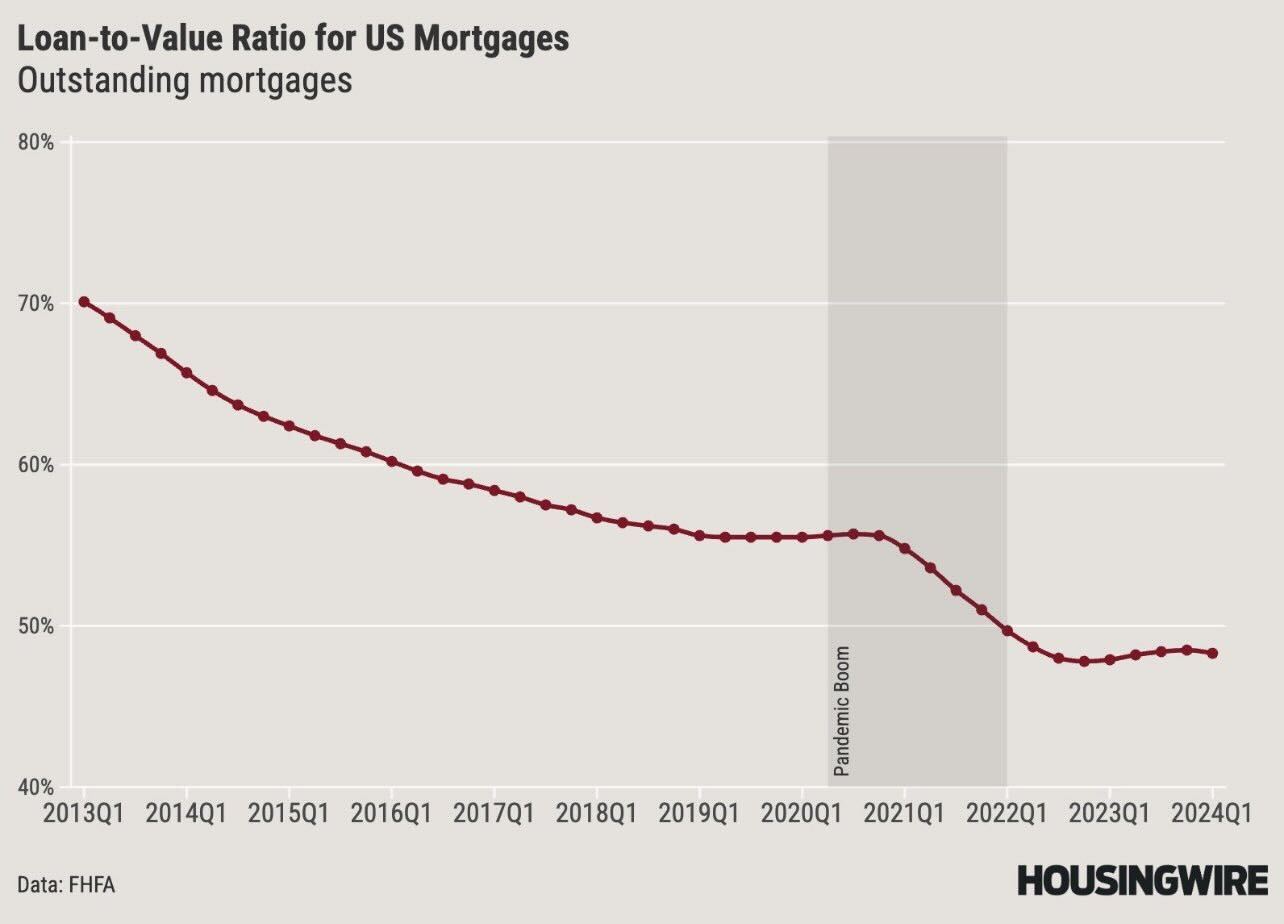

Something else to consider: over 40% of homes right now don’t even have a mortgage and the loan-to-value levels for those that do are under 50% on average. In 2008, the loan to value was nearly 85%. Also, the median downpayment data for this year is 15%, which means homeowners have more skin in the game than back then.

Hopefully, all these charts will clear up the confusion for your Uncle Dave or any other Thanksgiving guests who think we’ll see another housing crash like 2008. The credit data for homeowners tells a different story.

Categories

Recent Posts